This city is expensive, and it keeps getting more so. Wages haven't really kept up with rising prices, and Indonesia's middle class is shrinking — from 57.33 million people in 2019 to around 47.85 million today, a 16.54 percent drop that signals both tightening household budgets and a growing number of Indonesians falling out of the middle entirely.

It’s against this backdrop that working members of Generation Z are trying to build a career from the ground up, learning what adult life actually costs and relying on their own hard work — maybe for the first time — to fund the lifestyle they want. Every rupiah has to be earned, and in Jakarta, every rupiah has somewhere to go.

So how do people in their mid-20s actually make it work here? Not just survive, but build something? Three young Jakartans earning between Rp 10 and 20 million a month share what that looks like up close.

Rangga, 25: Save first, everything else follows

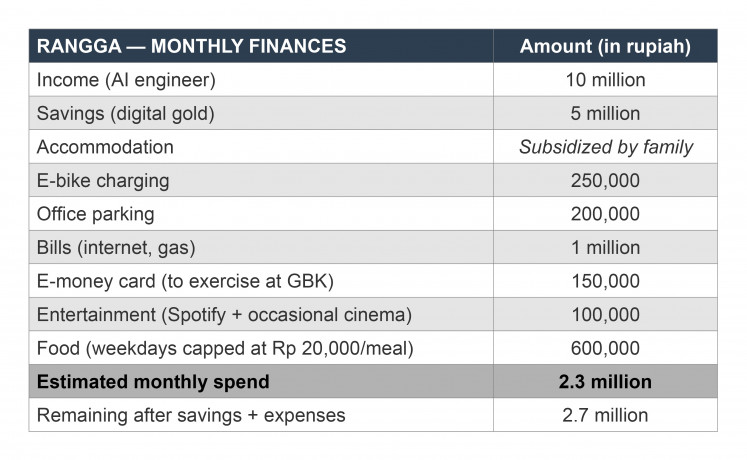

A mid-level artificial intelligence engineer in North Jakarta who caps his weekday lunch at Rp 20,000 (US$1.11), saves half his salary every month and is completely unbothered about it. The system works partly because of discipline, and partly because of a fortunate living arrangement he's the first to acknowledge.

Rangga earns around Rp 10 million a month and saves Rp 5 million of it every month, without negotiation, straight into digital gold. Whatever is left is what he has to live on. The math is tight, but for Rangga, that's the point.

Thank you!

For signing up to our newsletter.

Please check your email for your newsletter subscription.

"I cap myself at Rp 20,000 for food on weekdays so I won't stress about going out during the weekends," he says.

His operational expenses are lean and consistent: around Rp 250,000 to charge his e-bike, Rp 200,000 for office parking and about Rp 1 million for bills like internet and gas. For exercise, he loads Rp 150,000 onto an e-money card each month and works out at the Gelora Bung Karno stadium rather than paying for a gym membership. Entertainment is minimal, with just the occasional cinema trip and a Rp 50,000 Spotify subscription he's had for about a decade.

He is consciously frugal across the board, and he's clear about why. "I want to be frugal and save aggressively because I have goals. I want to buy my own car, I want to build a house eventually. So I have to be strict with my budget and savings. But I am horrible at tracking individual expenses," he says, laughing.

He also knows he has an advantage most people his age don't. His accommodation is owned by a family member, which means he pays no rent — a subsidy that makes his savings ratio possible in a way it wouldn't be otherwise. He doesn't downplay this. The system works, but it's built on a foundation that isn't available to everyone.

On the minimum wage question, Rangga is measured. For a single person without dependents, he thinks Rp 5.73 million is survivable. "I'm not saying it would be a comfortable life, but for one person, the minimum wage would get you by. With a tiny bit of savings too."

For actual comfort, he puts the figure around Rp 10 million. His personal ambition sits higher still — around Rp 40 million, the number he's decided would give him a family and a financially worry-free life.

Whether or not that number is realistic is something Rangga thinks about. "For my generation, having a house or getting married is still the signifier of success. We want to attain it, but it feels unreachable. The shift in priorities isn't out of will, it's because we know what's realistic and what's not."

Wawan, 27: The big spending umbrella

A consumer protection officer who saves 30 percent of his income before he does anything else, skips breakfast, splurges on protein at dinner and has a perfectly articulated answer for what a comfortable income looks like. Spoiler: it involves unlimited money.

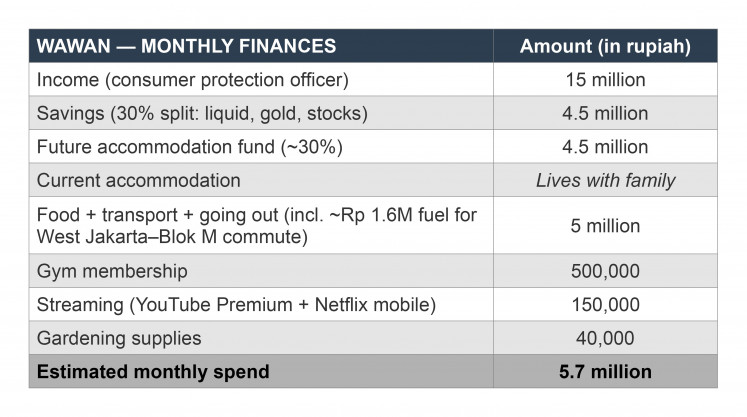

Wawan earns around Rp 15 million a month and, like Rangga, saves before he spends. His target is 30 percent — Rp 4.5 million — split across three buckets: a third stays liquid, a third goes into gold and the last third goes into riskier investments like stocks.

"I've read and watched a lot of financial guides and they all say you should set aside 20 percent to save. But like, what's another 10 percent? I don't spend that much anyways," he says.

Everything after savings falls under what he calls a big spending umbrella: a loose Rp 5 million monthly allocation that covers food, transport and going out. In practice, it rarely hits that ceiling. Weekday lunches run about Rp 20,000; dinners might reach Rp 50,000. "I skip breakfast, but I splurge a bit on dinners because I need the protein. And protein is expensive," he says.

The commute is his biggest variable cost. Wawan still lives with his parents in West Jakarta and works in the Blok M area — not an easy trip on public transport — so he drives, spending around Rp 1.6 million a month on fuel. He's thought about switching to a bicycle. "It's roughly an hour of cycling, and I spend an hour in my car already to drive, so I might as well get some exercise while I'm at it."

Other fixed costs include a Rp 500,000 gym membership and streaming subscriptions — YouTube Premium and the mobile-only Netflix tier — totaling around Rp 150,000 a month.

His only hobby is gardening, which he notes costs him roughly Rp 40,000 in fertilizer every now and then. "Maybe this comes from a place of privilege, but I don't really shop. If I already have five shirts for each workday, why would I buy another?"

The roughly 30 percent remaining from his income goes into what he calls his future accommodation fund — money earmarked for rent and other costs for a roof over his head that's closer to work. For now, it's just extra cash that he’s infusing into his savings.

Where Wawan diverges from Rangga is on the minimum wage question. He thinks Rp 5.73 million is simply too low. "There is a factor of people being irresponsible with their finances, driving the narrative of Jakarta being expensive. But regardless, I reckon Rp 5.73 million is just too low. You'd have to live insanely frugally and I wouldn't say that's humane. Sufficient, sure, but not good. Double that amount and then I think that's okay."

And his personal ideal income? He doesn't hesitate. "Unlimited money. I think that's the only right answer."

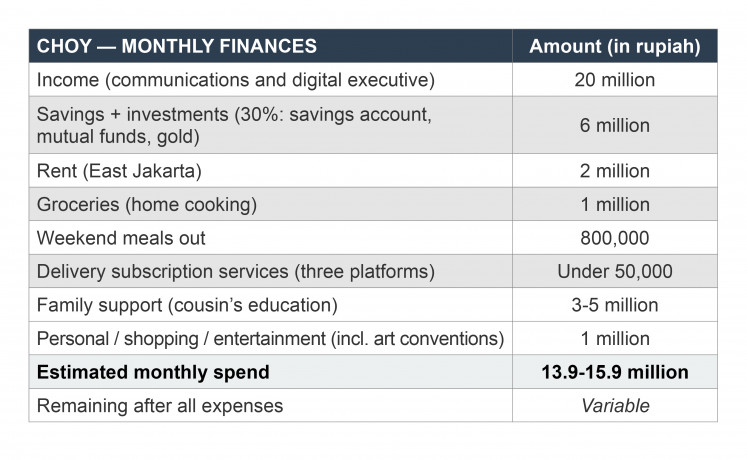

Choy, 27: Family first, then everything else

A communications and digital executive in East Jakarta who cooks her own lunches, supports a younger cousin through university and has organized her entire financial life around one nonnegotiable: that 30 percent goes to savings before she thinks about anything else.

Choy earns around Rp 20 million a month, the highest of the three, and lives in East Jakarta where rent runs Rp 2 million, significantly cheaper than the city's south and west.

She puts 30 percent straight into savings and investments each month, splitting it between a savings account and a mix of mutual funds and gold. "I think it is quite conventional to have most of your savings be money saved in a bank account. But that's how my parents taught me and I feel more comfortable with this portfolio because it's stable," she says.

Food is where Choy is most deliberate. She cooks most of her own meals, spending around Rp 1 million a month on groceries. For weekends, she allows herself around Rp 200,000 for a proper meal out.

When she's hanging out with friends and wants to order in, she relies on three delivery platform subscriptions that together cost under Rp 50,000 a month — a small fixed cost that unlocks free delivery and discount promos. "You get free delivery, you get a lot of promo discounts, it really does save me money for when I want to snack with my friends," she says.

Beyond her own expenses, Choy carries a significant family obligation: she transfers Rp 3 to 5 million a month to help her younger cousin through higher education. Sometimes that covers tuition, sometimes a laptop, sometimes both. "It's a routine I have to help take care of my family," she says simply.

Her recreational spending is the one place where she gives herself room. She doesn't budget strictly for personal or shopping expenses, letting them float at around Rp 1 million a month depending on what's happening. Art conventions are her main splurge — they happen a few times a year and she's comfortable spending up to Rp 1 million in a single day. "I like going to art conventions and that happens a few times a year, so I'm comfortable with splurging a bit."

The pattern that emerges across all her spending is less about what she spends and more about what she protects. The savings come first, the family commitment comes second. Everything else — food, entertainment, the occasional video game on sale — fits into what remains.

"What matters the most to me is my savings, paying the bills and my family," she says. "Maybe I can trim down on my spending on video games when they go on sale though," she adds with a laugh.

What's enough

None of them would say Jakarta is easy. But none of them seem particularly stressed about it either, which is maybe the more interesting thing.

The system each of them has isn't complicated: save first, build toward something specific and stop worrying about the rest. Rangga wants a car and eventually a house. Wawan wants unlimited money but in practice is fine with five shirts. Choy wants her cousin to finish school. Beyond that, they're not chasing much.

It helps, in Rangga and Wawan's cases, that neither of them is paying rent. The savings rates they've built would look different without that foundation, and both of them know it.

For their generation, as Rangga puts it, the shift in priorities isn't really a choice. It's just knowing what's realistic. That might sound like resignation, but looking at how these three have actually arranged their lives, it doesn't feel that way.

Aqraa Sagir is a writer for The Jakarta Post's Creative Desk. He’s chronically online in the hope it would be a useful asset for the job.